Boardwalk’s Expensive Lessons

The natural gas and NGL business has been lucrative for many MLPs. The Alerian Natural Gas MLP Index is an equal-weighted composite of 20 natural gas infrastructure MLPs that earn the majority of their cash flow from the transportation, storage, and processing of natural gas and NGLs. Over the past 12 months the index has had a total return of 14.2 percent, and presently yields 5.6 percent. And over the last five years, the index has enjoyed an impressive 301 percent total return.

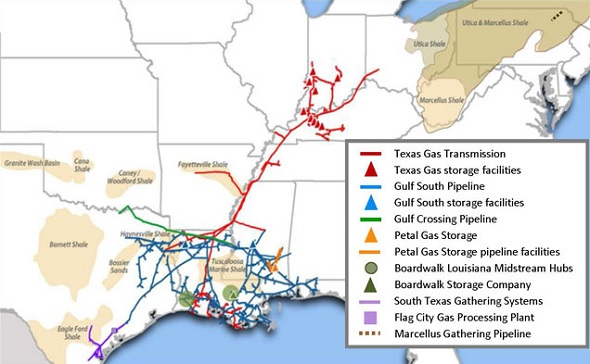

Boardwalk Pipeline Partners (NYSE: BWP) is a midstream partnership with a focus on natural gas and natural gas liquids (NGLs), and until recently one of the constituents of the Alerian Natural Gas MLP Index. The partnership operates 14,450 miles of pipelines and underground storage caverns with an aggregate working gas capacity of 207 billion cubic feet (Bcf) and liquids capacity of 18 million barrels.

Source: Boardwalk Pipeline Partners

Yet while the average natural gas MLP returned double digit gains over the past year, Boardwalk Pipeline Partners fell 52 percent. Year-to-date the partnership is down 45 percent, making it by far the worst performing of all MLPs so far in 2014. By comparison, the second worst performing MLP in 2014 is Natural Resource Partners (NYSE: NRP), down 19 percent on the year. Clearly something went horribly wrong at BWP.

It turns out that in addition to being in the right business segment, you also need to be in the right location. Boardwalk’s Texas Gas pipeline system had been living off legacy contracts that transported natural gas produced in Texas to the Midwest. But the Marcellus has now grown to become the largest natural gas producing play in the US, and gas from the Marcellus has been steadily making its way into the Midwest. As Boardwalk’s contracts have expired, renewals rates have been weak.

For those who listened to Boardwalk’s earnings calls last year, management provided plenty of signals that trouble loomed. On Feb. 10 those warnings culminated in a distribution cut of more than 80 percent, and Boardwalk’s unit price plunged by a steep 46 percent in a single trading session.

This was certainly unpleasant news for midstream MLP investors, who are accustomed to seeing relatively low volatility from this sector. But my colleague Igor Greenwald — who writes MLP Profits — provided a very prescient warning to sell Boardwalk on Nov. 15, 2013. In Walking Away From Boardwalk (for subscribers only), Igor wrote:

Boardwalk Pipeline Partners is a partnership with increasingly apparent profitability issues, driven chiefly by the fact that the Midwest and the East have nowhere near the same need for Texas gas now that production from the much nearer Marcellus and the Utica has glutted the regional market. Revenue would have declined on an organic basis excluding the effect of an acquisition, as gas transportation contracts were not renewed or renewed for less. Management estimated the bottom-line impact of this weakness in its core business at $40 million this year and as much again the next.

Meanwhile, sponsor Loews (NYSE: L) has added to the cash drain by converting its class B units into common that will cost Boardwalk an additional $25 million in distributions annually. The Bluegrass Pipeline Boardwalk is marketing in a partnership with Williams (NYSE: WMB) is looking more and more as a defensive measure to replace lost business than as a path to future glory. And it now faces competition that could drive expected returns lower.

Plus, increasingly profit-challenged Boardwalk will still need to finance its share of the cost for the Bluegrass. The distribution hasn’t increased in the last six quarters, and while the current 7.6 percent yield might look nice, next year’s distributable cash flow could be “well below” what it will take to keep it steady, Barclays recently noted in downgrading BWP to Underperform.

The unit price was down 10 percent on the month, and while it may be overdue for a bounce there’s no sense in sticking around on that basis. As a relatively recent recommendation by my predecessor, BWP shouldn’t impose major adverse tax consequences for those who followed the advice. And there are far better opportunities out there. Sell BWP.

Following that Sell alert, Boardwalk declined another 13 percent in the days leading up to Feb. 10, and then of course suffered the huge decline after the payout shocker. Units have since regained a small bit of ground, rising 8 percent from Feb. 11 through last Friday’s close.

The lesson from Boardwalk Pipeline Partners is to pay attention to changing business conditions, read the financials, and heed what management says on earnings calls. Many MLP investors will likely never trust Boardwalk again, but this is simply a case where changing business conditions caused dwindling cash flow, and it was clearly no longer projected to meet the expected distribution.

Boardwalk’s story is far from over. Now that management has made a drastic distribution cut in order to preserve the future of the partnership, it should once more be evaluated based on the current unit price and forward prospects. (Igor took another detailed look at the “new” Boardwalk in the latest MLP Profits.)

(Follow Robert Rapier on Twitter, LinkedIn, or Facebook.)

Portfolio Update

A Chill Wind Off the Baltic

A reader recently asked about Navios Maritime Partners (NYSE: NMM) and the factors that drive its typically volatile unit price. Although the bulk shipper’s revenue is protected against short-term fluctuations in commodity shipping rates. its market performance remains highly sensitive to the performance of the Baltic Dry Index, especially its Panamax and Capesize components.

The Baltic Dry Index is down 44 percent since the first close of 2014, done in above all else by gathering evidence of an industrial slowdown in China as the world’s longtime growth engine copes with pollution and a private-sector credit crunch.

Sentiment for the emerging markets that account for the lion’s share of the global shipping has been weak for much of 2014, though that’s recently begun to change for India as well as Brazil.

Despite the Baltic Dry’s slump, NMM’s unit price has slipped all of 1 percent since Jan. 2, on management warranties that the $1.77 annual distribution is locked in through the end of 2015, and hopes that it might rise from there. That’s a reflection of the shipping rates’ current global ebb, which long ago reached the point of encouraging fleet capacity cuts, as well as the company’s strong portfolio of profitable long-term charters.

Our price target remains at the low end of the recent trading range and a level sufficient to deliver a 10 percent yield at the current payout. Buy NMM below $17.70.

— Igor Greenwald

Stock Talk

Jackpine Savage

I have a large return of Cont. coming in May where would you put this money? EPD,ETE,OILT?

Igor Greenwald

EPD and ETE are two of our favorite holdings; EPD, which is the more conservative investment, is our top-ranked Best Buy.

You must be logged in to post to Stock Talk OR create an account

You must be logged in to post to Stock Talk OR create an account

Add New Comments

You must be logged in to post to Stock Talk OR create an account