Holy Holly, What a Deal

The monthly joint web chat for subscribers of The Energy Strategist (TES) and MLP Profits is typically conducted on the second Tuesday of each month. This chat is conducted by Igor Greenwald, managing editor for TES and chief investment strategist for MLP Profits, and myself. This past week, the Mother’s Day snowstorm in Colorado caused me to miss the chat for the first time ever. I want to thank Igor for carrying on with the chat, and I apologize to subscribers for missing it.

Igor addressed all of the MLP-related questions during the chat, but there was one which warrants some elaboration. It will be the subject of today’s column.

Q: Any thoughts on Holly Energy Partners? With a 6% yield, 6.4% annual dividend growth, and mostly fee-based revenue, it looks interesting here.

Over the past few years there has been a trend of oil refiners spinning off their midstream assets — that is to say the assets involved in logistics such as pipelines and storage tanks — into master limited partnerships (MLPs). The way this works is that the refiner sells, or “drops down” these assets into the MLP, which typically has preferred access (such as a right of first refusal on the partner refiner’s assets). Because of the tax-advantages gained from the MLP structure, these assets will then trade at a premium relative to the valuation of the refiner, which enables the sponsor to unlock shareholder value.

Just to name a few refiners that have taken this route:

Tesoro Corporation (NYSE:TSO) formed Tesoro Logistics (NYSE: TLLP) in 2011.

Phillips 66 Partners (NYSE: PSXP) was the hottest IPO of 2013, and is made up of midstream assets dropped down from its sponsor, the refiner Phillips 66 (NYSE: PSX).

Western Refining Logistics (NYSE: WNRL) went public in Q4 2013 with midstream assets acquired from Western Refining (NYSE: WNR).

All of these spin-offs have performed well. WNRL is up 45 percent since its IPO, PSXP has doubled since its IPO, and TLLP has returned nearly 200 percent in the three years since its IPO.

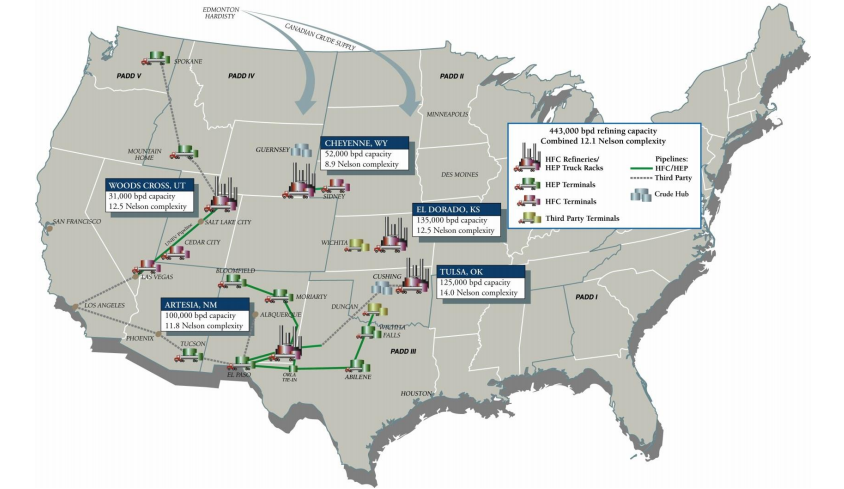

But these are all Johnny-come-latelies compared with Holly Energy Partners (NYSE: HEP), which was formed in early 2004 by HollyFrontier (NYSE: HFC). HollyFrontier owns (through subsidiaries) 37 percent of HEP through limited partner interests and 2 percent through a general partner interest — and has 443,000 barrels per day (bpd) of crude oil refining capacity scattered across the West and the Midwest.

Source: HFC investor presentation

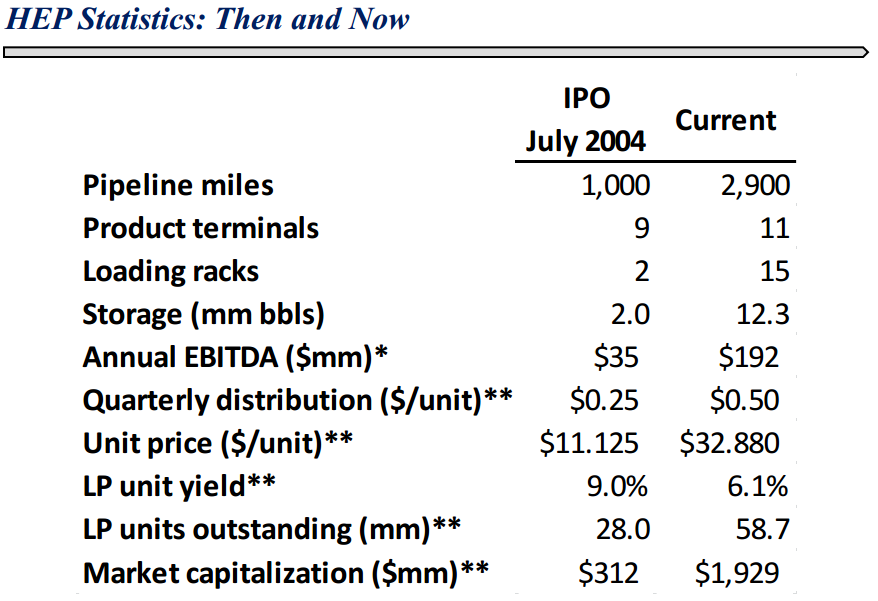

Since 2004, Holly Energy Partners has been growing through capacity expansions and acquisition of third-party midstream assets (and not only from HFC). The partnership has averaged more than one project/acquisition per year since its IPO. These acquisitions have led to a near tripling of the partnership’s pipeline miles (from 1,000 in 2004 to 2,900 by 2013) and have increased storage capacity sixfold to 12 million barrels.

Source: HEP investor presentation

Over that same period since its IPO, HEP has grown annual EBITDA from $35 million to $192 million. The per-unit distribution has doubled, but MLPs across the board had enormous capital appreciation over the past decade. Thus, the unit price outpaced the distribution increase (and the increases in EBITDA) such that the annual yield has declined from 9 percent in 2004 to 5.9 percent at the closing price on May 16.

Source: HEP investor presentation

All of HEP’s revenue is fee-based (in other words, it has no direct commodity risk), and over 80 percent of the partnership’s revenues are backed by long-term contracts and minimum commitments. The minimum commitments produce more than $259 million in annual revenue, approximately $225 million of which comes from contracts with HollyFrontier.

Revenue for the first quarter 2014 was $87 million, a $12.7 million increase in a year’s time. The revenue breakdown was:

Revenue from refined product pipelines was $35.8 million, an increase of $8.7 million compared with the first quarter of 2013

Revenue from intermediate pipelines was $7.9 million, an increase of $1.7 million compared with the first quarter of 2013

Revenue from crude pipelines was $12.6 million, an increase of $1 million from the first quarter of 2013

Revenue from terminal, tankage and loading rack fees was $30.7 million, an increase of $1.3 million year-over-year

Net income attributable to Holly Energy Partners for Q1 was $24.1 million, versus $18.4 million in the first quarter of 2013. Overall pipeline volumes were up 22 percent versus Q1 2013.

On the basis of the first-quarter results HEP announced its 38th consecutive distribution increase, raising the quarterly distribution to $0.5075 per unit, which is a 6.3 percent increase over the distribution for the first quarter of 2013. The partnership has raised the distribution in every quarter since going public in 2004.

Given the impressive track record since the IPO, the yield stability imparted by the exclusively fee-based contracts, and a yield that is still near 6 percent, I have to agree that Holly Energy Partners certainly looks interesting.

(Follow Robert Rapier on Twitter, LinkedIn, or Facebook.)

Portfolio Updates

Williams Never Better

It’s been a great spring for MLPs, and as we approach the one-year anniversary of last year’s selloff on worries about rising rates, the sector shows few signs of slowing down.

General partner sponsors of master limited partnerships have been leading this parade, on expectations that they will pocket more of the upside via incentive distribution rights and fully valued asset dropdowns.

#5 ranked Best Buy Williams (NYSE: WMB) has been among the major beneficiaries of this trend, and has now returned 30 percent since our Buy recommendation in October.

Today the stock is at a record high after the company announced at its annual analyst day last week that prior guidance for distribution growth of 20 percent annually through the end of 2015 has now been extended through the end of 2016, with “high coverage and line of sight to growth beyond.”

Williams also has a plan to “transition … toward pure-play GP holding company,” which would mean dropping down the rest of its directly held assets to MLP affiliate Williams Partners (NYSE: WPZ).

The share price has just exceeded a price target raised only recently, which we’ll likely raise in due time. For now, buy WMB on dips below $46.

Two Votes of Confidence in Kinder Morgan

Will the investors enthusiasm for most energy plays lift Kinder Morgan (NYSE: KMI) from the vicinity of two year lows one day soon. We certainly expect so, after upgrading KMI to Buy from Hold a month ago on the increasingly apparent growth prospects in its affiliated MLP’s core gas transmission business.

Last week the analyst at Goldman Sachs made a similar call, adding Kinder Morgan to thje firm’s “Conviction Buy List” for similar reasons. More importantly, founder Richard Kinder continued to increase his stake ahead of the annual shareholder meeting and an industry conference this week, spending another $3.2 million on May 9 to increase a $7.7 billion position to which he has committed the bulk of his fortune.

Kinder’s record and his persistence in buying KMI shares are hard to bet against. Continue buying KMI below $37.

— Igor Greenwald

Stock Talk

Add New Comments

You must be logged in to post to Stock Talk OR create an account