Upstream or Up the Creek?

Most master limited partnerships (MLPs) operate in the “midstream” portion of the oil and gas business. “Midstream” refers to the transportation of oil and gas, and these midstream MLPs collect fees for providing the pipelines, storage tanks, etc. that move oil and natural gas from the production site to market.

Midstream partnerships have less commodity exposure than “upstream” MLPs, which are those focused on the extraction of oil and gas. Because of the commodity exposure, investing in upstream MLPs entails more risk, but they also generally have higher yields than their midstream counterparts. While most midstream MLPs have yields in the 4% to 6% range, upstream MLPs commonly yield in the 8% to 12% range.

But higher risk means more potential for losses when the markets turn against you. Declining commodity prices hurt the bottom line of upstream MLPs, and thus their ability to maintain or grow distributions. Most upstream MLPs use hedging to some degree to limit the commodity risk, but ultimately falling commodity prices will drag down their performance.

Because oil and gas prices do not always trade in tandem, upstream partnerships can behave very differently based on the relative percentage of a partnership’s production in oil and gas.

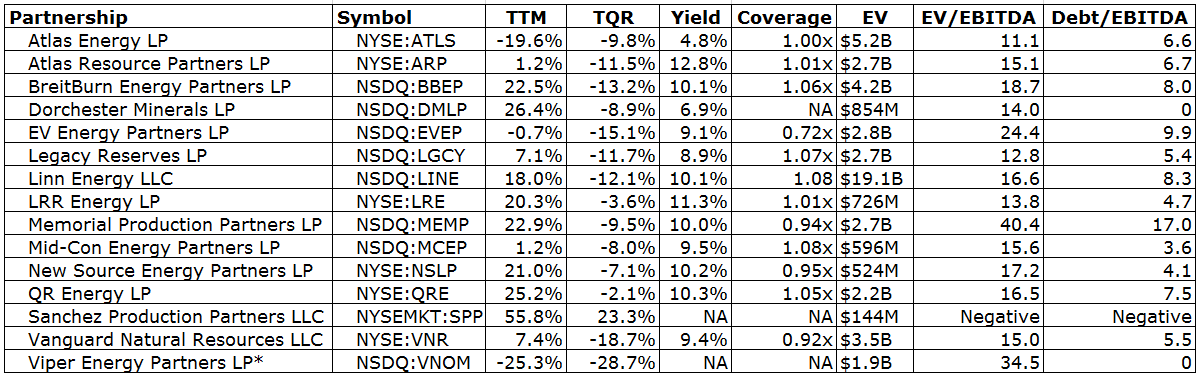

According to the National Association of Publicly Traded Partnerships (NAPTP), there are 15 publicly traded partnerships engaged primarily in upstream operations. Most of these are engaged in oil and gas production, but Viper Energy Partners (NASDAQ: VNOM) owns mineral rights and relies on royalty payments for distributions.

*VNOM conducted its IPO on 6/18/14

TTM = Trailing Twelve Month total return through midday on 10/06/14

TQR is the total return over the past three months

Coverage = Cash available for distribution divided by cash distributed

EV – Enterprise Value in billion dollars on 10/06/14

EBITDA = Earnings Before Interest, Taxes, Depreciation and Amortization (TTM)

Debt/EBITDA = Ratio of total debt to TTM EBITDA

Except for Sanchez, all of these partnerships had positive earnings before interest, taxes, depreciation and amortization (EBITDA) over the past year. The average total return of the group for the past 12 months is +12.2%, with an average yield of 9.5%. But over the past 3 months as the price of West Texas Intermediate fell from near $105/barrel (bbl) to its current price around $90/bbl — a decline of 14% — the average upstream partnership has declined by 9.1%.

Natural gas prices have held up better than oil prices in recent months. Natural gas is more subject to seasonal pricing, but relative to a year ago natural gas prices are about 10% higher (while WTI was still over $100/bbl a year ago). Thus, the upstream partnerships with a higher percentage of overall production in natural gas will probably have an easier time maintaining distributions in the third and fourth quarters.

Investors looking for bargains in the upstream MLP sector should pay attention to the coverage ratios as third quarter distributions are announced. A significant deterioration in the coverage ratio could indicate that an upstream MLP is insufficiently hedged, and/or has a high percentage of its production as oil during this period of falling oil prices. MLPs whose coverage ratios hold up well would be near the top of my list for consideration, particularly if they are not overleveraged relative to their peers.

(Follow Robert Rapier on Twitter, LinkedIn, or Facebook.)

Portfolio Update

Targa Keeps Growth Plans on Track

With crude futures beaten down to 18-month lows and some of the riskier shale drillers trading as if they might never drill another well, midstream processors and shippers have been a relatively safe harbor for energy investors. These companies, which have their ear to the ground in all the key shale plays, are pushing ahead with growth plans, a hopeful sign for a market desperately in need of some.

On Monday, Targa Resources Partners (NYSE: NGLS) said it would buy and install two more cryogenic gas processing plants, a 300 million cubic feet per day (MMcf/d) one on the western end of the Permian Basin in Texas, and a 200 MMcf/d facility serving the Bakken drillers in North Dakota. The latter is set to come online late next year, while the Texas plant is expected to be operational in early 2016. Since gas production in the Permian and the Bakken has been largely incidental to crude exploration, Targa clearly believes the recent correction won’t significantly alter its customers’ growth plans.

The partnership’s units have traded in a tight range since its parent rejected takeover interest from Energy Transfer Equity (NYSE: ETE) earlier in the year, and the current 4.6% yield on a distribution recently growing as much as 10% a year still provides plenty of value. NGLS remains a hold for subscribers who took our advice to lighten their positions when it was trading 5% above the current price in late June.

— Igor Greenwald

Stock Talk

az boy

Igor,

What happened to the safety ratings………………

Lots on this list are far below recent buy ratings…………..

Time to deliver buy / sell / hold info ……………….

Telling us to evaluate coverage ratios……….What do we pay you for ????????????????????

You must be logged in to post to Stock Talk OR create an account

Add New Comments

You must be logged in to post to Stock Talk OR create an account