The Bad and the Ugly of 2014

Here at the end of the year, I like to look back at the top and bottom performing master limited partnerships (MLPs) since Jan. 1. The year was extremely volatile for the entire energy space, and MLPs were not spared. The severe price drop hit upstream MLPs especially hard. In fact, all but two of the 10 worst-performing MLPs for the year were in the upstream sector. Since there are still a few trading days left in the year the list may change slightly, but is unlikely to change substantially.

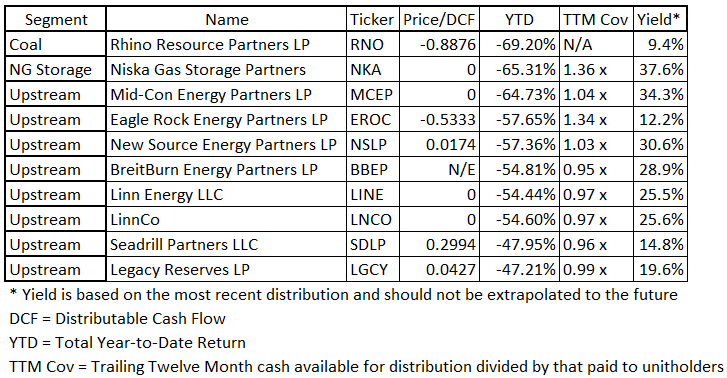

Here are the 10 worst performers for the year to date through Dec. 19, followed by commentary on the bottom five. Data is courtesy of MLP Data.

First, do note that these yields are based on distributions made under better business conditions than those prevailing currently. The deteriorating conditions have depressed unit prices, making the yields look much better than they are likely to be going forward. Most of these MLPs will likely see distribution cuts.

The worst performer for the year has been Rhino Resource Partners (NYSE: RNO), with a loss of 69.2%. This partnership is in the coal business, and that’s been in the dumps for a few years now. In October, RNO announced a large distribution cut, and unit prices plummeted.

Niska Gas Storage Partners (NYSE: NKA) is down 65.3% YTD. The partnership has been plagued by earnings disappointments and declines in its fixed-fee revenue. On the conference call discussing the most recent quarterly results, the CEO warned that “in light of the continuing challenging conditions in the natural gas storage market, the board is reviewing the distribution level going forward and it is likely that the distribution will be reduced beginning this fiscal third quarter or suspended if current market conditions persist.”

The next three on the list, Mid-Con Energy Partners (NASDAQ: MCEP), Eagle Rock Energy Partners (NASDAQ: EROC), and New Source Energy Partners (NYSE: NSLP) were down respectively 64.7%, 57.7%, and 57.4% respectively. These three partnerships are all engaged in the production of oil and gas. Even though most of Eagle Rock’s production is natural gas, a 2013 distribution cut and the subsequent suspension of the distribution helped drive down the unit price over and above the decline due to commodity prices.

While 2014’s big losers were concentrated in the upstream sector, there were still plenty of winners in 2014. Like the losers, the winners have a few things in common. I will discuss the top 10 MLPs of 2014 in next week’s issue.

(Follow Robert Rapier on Twitter, LinkedIn, or Facebook.)

Portfolio Update

Memorial Buyback Aims to Buy Low

While upstream MLPs have been among the year’s worst performers, recent portfolio addition Memorial Production Partners (NASDAQ: MEMP) has rallied nearly 20% off its Dec. 15 low, aided by Thursday’s announcement of a $150 million common unit buyback.

The move is a reflection of MEMP’s unusually strong liquidity and its best-in-class hedging program, which protects almost all of the partnerships profits for at least the next three years. For those reasons, Memorial remains an attractive bottom-fishing opportunity. MEMP is an Aggressive Portfolio buy below $15.

— Igor Greenwald

Stock Talk

Mr. Ed, The Talking Horse

Igor, thank you for the MEMP pick, and some of the other ideas resulting from the general drop. Much appreciated.

Igor Greenwald

Thanks for the kind words and your business, Ed. I did a little traveling around the holidays but am back and hoping for better news in the new year.

You must be logged in to post to Stock Talk OR create an account

You must be logged in to post to Stock Talk OR create an account

Donald Christensen

No comments on Breitburn Energy? QRE was looking good until October/November. When merged with Breiburn it really hit the fan. Why?

Don C, Florida

Igor Greenwald

When we recommended VNR and MEMP last month, it was on the premise that these were the two upstream MLPs most insulated from the fall in commodity prices. Everything that’s happened since, including last week’s big distribution cuts by Breitburn and Linn, argues that we made the right choice. Breitburn and Linn unit prices actually rose on the news, so the market was obviously already pricing in a lot of short-term pain. But we’re still much more comfortable with Vanguard and Memorial as rebound plays; Memorial’s hedges provide much more protection, and Vanguard’s a relatively low-cost operator forcused on natural gas.

You must be logged in to post to Stock Talk OR create an account

You must be logged in to post to Stock Talk OR create an account

Add New Comments

You must be logged in to post to Stock Talk OR create an account