The Natural Gas Oversupply And How To Play It

North American natural gas prices should remain at depressed levels throughout the fall and could decline even further as hurricane season draws to a close. The reason is simple: US natural gas output continues to outstrip demand.

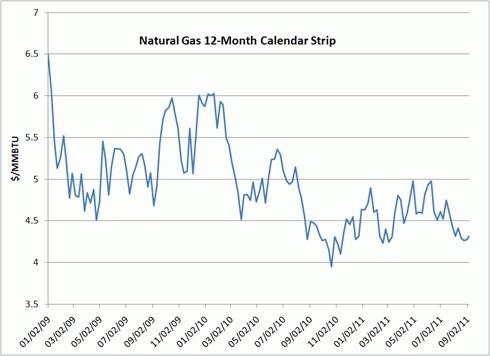

In my Jan. 7, 2011, InvestingDaily.com article, Special Edition: 2011 Forecast, I called for natural gas prices to remain range-bound in 2011; this forecast has panned out thus far. Check out this graph of the 12-month strip for natural gas prices at the Henry Hub. The average of the next 12 months of futures prices, the 12-month strip, eliminates some of the inherent seasonality in gas prices and approximates the average price a gas producer with no hedges would receive for its full-year output.

Source: Bloomberg

Although the 12-month strip price for natural gas prices generally has hovered between $4 and $5 per million British thermal units (BTU), the long-term outlook for demand and pricing remains favorable.

The cleanest-burning fossil fuel, natural gas should continue to win market share from coal, a transition hastened by stricter restrictions on carbon dioxide (CO2) emissions. Given the opposition to the construction of new nuclear reactors, natural gas-fired plants remain the best option to boost baseload power while reducing the amount of CO2 released into the atmosphere.

Meanwhile, the relative abundance of natural gas in the US could eventually lead to increased fuel switching in the transportation sector. Natural gas-powered vehicles (NGV) have already made inroads into taxi and bus fleets and caught on in the waste-management industry. Have a look at this InvestingDaily.com article for a great read on NGVs.

But the game changer for US natural gas demand would be increased adoption of NGVs in the commercial trucking industry. Although this transition would reduce energy costs and CO2 emissions, the amount of infrastructure investment needed to support widespread adoption of NGVs in the US is a significant challenge that will take some time to overcome.

Over the past few years, politicians and industry leaders occasionally hype the prospect of legislation that would subsidize the use of natural gas as a transportation fuel. When that happens NGV-related stocks enjoy a short-live bump. For example, Westport Innovations, a firm that makes natural gas-powered engines, surged from $19 in late March to $28 per share in early April after President Obama delivered a speech that highlighted natural gas as a crucial component of the nation’s energy independence.

Don’t believe the hype. With a contentious election looming on the horizon and lawmakers focused on cutting spending, a transformational bill such as the New Alternative Transportation to Give Americans Solutions Act (NAT GAS Act) stands scant chance of passing.

Disconcerted by the breakdown between domestic natural gas prices and drilling activity, North American commentators tend to regard global markets for liquefied natural gas (LNG) as a potential outlet for production from the continent’s prolific shale gas fields.

On May 20, 2011, the US Dept of Energy granted Cheniere Energy permission to export as much as 2.2 billion cubic feet of LNG per year. LNG is a super-cooled form of natural gas that can be easily transported via specialized tankers to any country with import (regasification) terminals. For more on how the LNG market is reshaping the global economy, check out my Seeking Alpha article here.

Although the Kenai LNG port in Alaska is the nation’s sole export terminal, the US is home to several import facilities. Built before the shale gas revolution transformed the US market, these liquefaction terminals operate at a fraction of their capacity because the country no longer needs to import LNG. Several of these operators have received approval to re-export LNG imported from other regions for temporary storage in the US, but these modest volumes don’t come close to making up for lost imports.

Cheniere Energy’s stock popped after the Dept. of Energy approved the company’s export application, rallying almost 50 percent in only a few days. The company may have some of the regulatory approvals in hand–the Federal Energy Regulatory Commission has yet to approve the site plan officially–but adding liquefaction capacity to the company’s Sabine Pass import terminal will require substantial investments of time and capital.

The firm’s construction plan involves two phases, each of which will cost $3 billion to complete–a tall order for a company with a market capitalization of $500 million and almost $3 billion in existing debt. Even in the best circumstances, the first phase of the project wouldn’t be operational until 2015 or 2016. Meanwhile, potential LNG exports of 2.2 billion cubic feet per day will barely cause a ripple in a US natural gas market that amounts to roughly 60 billion cubic feet per day.

Not only are US LNG exports highly unlikely to provide a meaningful release valve for the nation’s current supply overhang, but investors should also steer clear of names whose growth prospects depend entirely on planned liquefaction terminals.

Stock Talk

Add New Comments

You must be logged in to post to Stock Talk OR create an account