Crude Realities And The Price Of Oil

Crude oil prices remain elevated because of a tight supply-demand balance. Let’s look at the supply and demand sides of the equation.

Some investors still ask me why oil prices remain high even though demand is weak. This question assumes that sluggish growth in the US and other developed economies necessarily vitiates oil demand.

In 2010 the world consumed about 88.2 million barrels of oil per day–2.7 million barrels per day more than in 2009. Whether you look at the incremental increase in demand or the percentage gain, oil demand in 2010 increased at the second-fastest pace in 30 years. Much of this rebound stemmed from the snap-back in consumption that followed the severe 2008-09 recession. But the magnitude of this recovery took many analysts and industry participants by surprise.

Investors should also remember that although US oil demand remains well under its 2004-05 high, global oil demand hit a new peak in 2010. Demand growth in 2011 won’t match up with last year’s resurgence. However, the International Energy Agency’s (IEA) forecast still calls for global oil demand to grow by more than 1 million barrels per day to 89.3 million barrels per day. This uptick in consumption hardly qualifies as weak; oil demand has grown at an average annual rate of 1.05 million barrels per day since 1990.

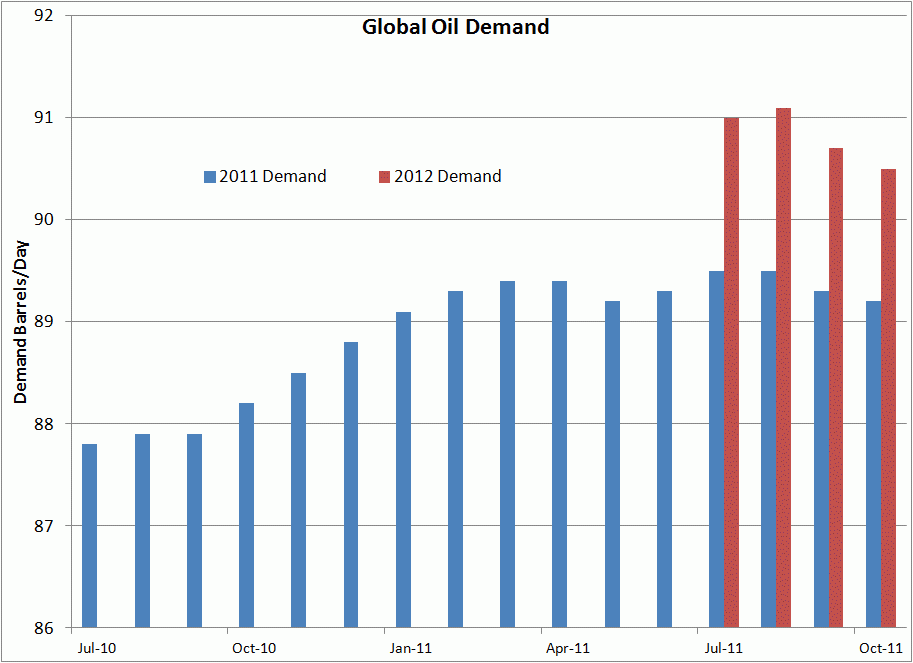

The IEA has raised its estimate of 2011 crude oil demand sharply higher since July 2010. Although the agency has trimmed its projection by about 300,000 barrels per day since August, these estimates remain far higher than they were six months ago.

(Click charts to expand)

Source: International Energy Agency

The IEA first published its estimate of 2012 global oil demand in July and has steadily reduced this projection by roughly 500,000 barrels per day. Even with these revisions, global oil demand is expected to expand by 1.3 million barrels per day. If this scenario pans out, global oil demand would exceed 90 million barrels per day for the first time in history.

Of course, accurately forecasting global oil demand is at best an inexact science that inherently entails multiple revisions. Signs of economic weakness in the US and emerging markets have prompted IEA economists to lower their estimates of 2011 and 2012 oil demand.

Oil prices also factor into the IEA’s revisions. When oil prices are elevated, demand growth invariably slows.

Since the US and other developed economies hit a soft patch in spring, the risk to global economic growth skewed to the downside. At the same time, oil prices remained elevated. These factors prompted me to call for crude oil prices to drop from sky-high levels in the April issue of the Energy Strategist:

Recent developments [unrest in the Middle East and North Africa] suggest that oil prices will easily average more than $100 per barrel in 2011. Investors also shouldn’t rule out a move to $140 per barrel at some point this year–a price point I had expected in 2012. I see a 50-50 chance that oil breaches $140 per barrel in 2011. As before, Brent crude oil will lead any rallies; WTI should continue to trade at a discount to Brent for the foreseeable future. But don’t expect Brent crude oil to remain above $120 per barrel for a prolonged period, as demand growth would suffer.

Contrary to popular belief, sky-high oil prices aren’t welcome news for energy producers, oil services companies and other stocks in the energy patch. Although profits may jump in the short term, inordinately high oil prices tend to erode global demand and set the stage for a correction. Producers would prefer that oil prices hover around $100 per barrel, a sustainable level that generates solid profits and encourages drilling activity. Fears of demand destruction are one of the main reasons energy stocks fall or rally only slightly when oil prices jump.

This view has largely proved correct. Brent crude oil topped out near $130 per barrel and WTI had continued to trade at a historically high discount to its counterparts. The price of Brent crude also pulled back over the summer, though the benchmark never breached $100 per barrel. Oil prices should average north of $100 per barrel this year.

Don’t expect another run-up in Brent crude oil prices this year: Economic growth remains sluggish in developed nations, and oil prices are still high enough to generate some meaningful demand destruction.

By the same token, I don’t foresee much additional downside for oil prices in early 2012 because economic risks have receded. As I wrote in The Case of Adding Risk, US gross domestic product likely grew at the fastest pace in the third quarter since the second half of 2010.

China’s economic growth has decelerated to a 9.1 percent annualized pace, a sustainable rate which suggests that policymakers successfully curbed speculation and inflationary pressures. Look for Beijing to stop tightening monetary policy and to start taking steps to promote growth by early 2012.

Source: International Energy Agency

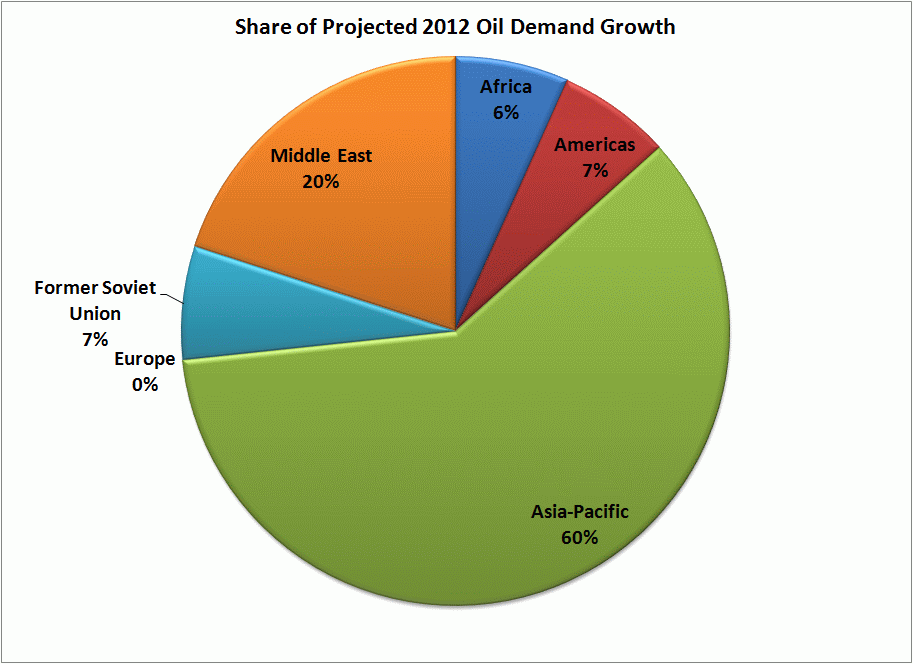

I break down the outlook for oil demand in the Americas and emerging markets in the mid-October issue of The Energy Strategist.

Now that we’ve gotten the demand view, let’s examine the outlook for oil supply.

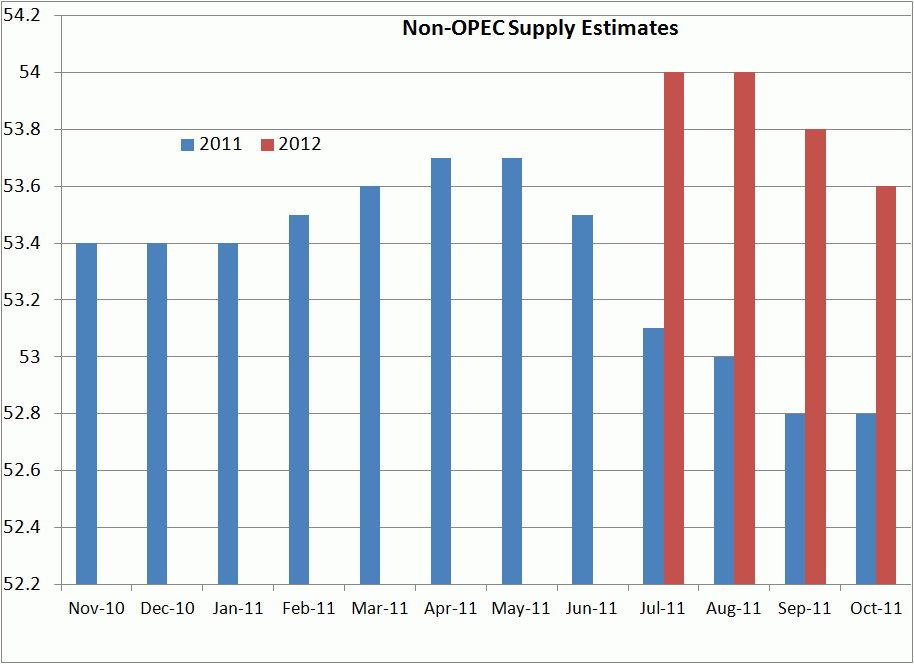

The IEA has slashed its estimate of non-OPEC oil production at an even faster pace than reduced its forecast for oil demand.

Source: International Energy Agency

This graph shows the IEA’s estimates of non-OPEC oil output for 2011 and 2012. The agency issues its initial estimate for the following year in July and revises this projection as warranted.

Since May, the IEA has lowered its forecast of 2011 non-OPEC production by 900,000 barrels of oil per day to 52.8 million barrels per day. This projection implies year-over-year non-OPEC production growth of only 200,000 barrels of oil per day.

If global oil demand expands by forecast 1 million barrels per day in 2011, non-OPEC production will satisfy only 20 percent; OPEC will need to ramp up production or countries will need to dip into their stockpiles.

Global oil inventories have declined relative to 2010 levels, but these reserves won’t fill the gap. This imbalance–exacerbated by the loss of Libya’s 1.5 million barrels per day of light, sweet crude oil for six months–forced OPEC to tap into spare productive capacity to cap prices and limit demand destruction.

Investors should pay close attention to OPEC’s spare capacity when divining oil prices. In general, oil prices tend to rise when OPEC’s spare capacity declines.

At the end of 2010, effective OPEC’s spare capacity stood at 5.6 million barrels of oil per day. Today, sluggish non-OPEC output growth, rising demand, and supply disruptions have reduced the cabal’s spare capacity to 3.25 million barrels of oil per day. This single statistic tells you a lot about why oil prices have been resilient this year.

Spare capacity should remain tight. Libya’s oil production may recover to between 200,000 and 300,000 barrels per day by early 2012 But the Libyan government has admitted that production won’t return to pre-conflict levels before early 2013.

Meanwhile, the IEA has lowered its estimate of 2012 non-OPEC production by 400,000 barrels of oil per day. Expect OPEC’s spare capacity to dwindle throughout 2012.

I foresee more downside risk to the IEA’s non-OPEC supply estimates than I do for global oil demand. Producers increasingly have to target complex, expensive-to-exploit fields in the deepwater and other remote areas to generate incremental output growth. Drilling activity has also increased in unconventional plays such as North America’s shale oil and gas fields and Canada’s oil sands.

The balance between global oil demand, supply and spare capacity remains tight. Higher oil prices are necessary to incentivize the development of complex fields. Higher prices are also the only way for the global oil market to effectively limit demand; if consumption growth in 2012 matched the IEA’s estimate for 2011 demand growth, the world’s spare capacity would be effectively eliminated.

Based on this outlook, I continue to favor oil services names like Weatherford International (NYSE: WFT) and Schlumberger (NYSE: SLB), which have pulled back because of the recent growth scare and EU sovereign-debt crisis–not the realities of the global oil market. I profiled Weatherford International in an August 2011, article for Seeking Alpha.

Stock Talk

Add New Comments

You must be logged in to post to Stock Talk OR create an account