High Plains Lifters

Despite the recent carnage in the energy markets, some segments have continued to perform well. I have stated on many occasions that I am bullish on long-term natural gas prices, in large part because of liquefied natural gas (LNG) terminals that will begin exporting gas during the next five years. And natural gas prices have held up well during the sell-off. While oil prices have declined by a third in the past 12 months, natural gas prices are within 5% of their value a year ago.

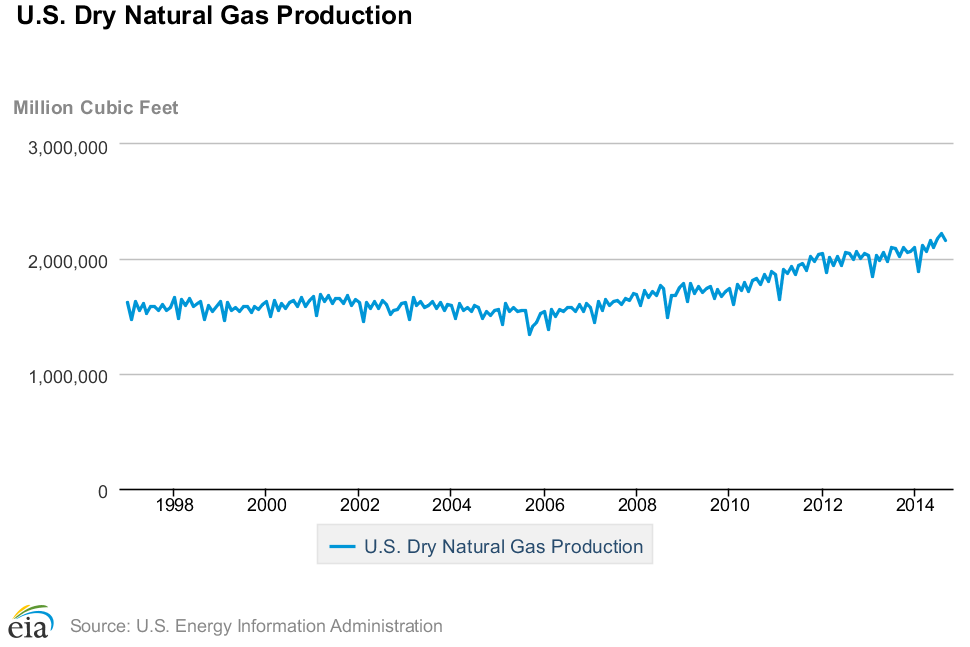

The ongoing shale gas boom continues to push U.S. natural gas production to new records:

But this natural gas needs to get to market, and that’s where it pays to have natural gas pipelines in the right locations. Two of the top five MLPs by market returns year-to-date (YTD) are natural gas pipeline companies. TC PipeLines (NYSE: TCP) is an affiliate of TransCanada (NYSE: TRP, TSE: TRP), and has a total YTD return of 65%.

TCP has investments in more than 5,500 miles of regulated interstate natural gas pipelines with a combined capacity of 8.9 billion cubic feet per day (bcf/d), accounting for 8% of the U.S. daily gas shipments volume. Revenues from these assets are derived almost entirely from fee-based contracts.

TCP Pipelines’ assets. Source: TCP website.

TC PipeLines has stakes in the following assets:

46.45% of Great Lakes, a 2,115-mile pipeline that connects with the TransCanada Mainline at the Canadian border near Emerson, Manitoba, Canada and St. Clair, Michigan, near Detroit. Great Lakes is a bi-directional pipeline that can receive and deliver natural gas at multiple points along its system. TransCanada owns the remaining 53.55% of Great Lakes;

50% of Northern Border, a 1,408-mile pipeline that connects from the Canadian border near Port of Morgan, Montana to a terminus near North Hayden, Indiana, south of Chicago. Northern Border is capable of receiving natural gas from Canada, the Williston Basin and Rocky Mountain Basin. ONEOK Partners (NYSE: OKS) owns the remaining 50% of Northern Border;

70% of GTN, a 1,353-mile pipeline that extends between an interconnection near Kingsgate, British Columbia at the Canadian border to a point near Malin, Oregon at the California border and delivers natural gas to the Pacific Northwest and to California. TransCanada owns the remaining 30% of GTN;

100% of Bison, a 303-mile pipeline that extends from a location near Gillette, Wyoming to Northern Border’s pipeline system in North Dakota. Bison transports natural gas from the Powder River Basin to Midwest markets. TransCanada owns the remaining 30% of Bison;

100% of North Baja, an 86-mile pipeline that extends between an interconnection with the El Paso Natural Gas Company pipeline near Ehrenberg, Arizona and an interconnection with a natural gas pipeline near Ogilby, California on the Mexican border. North Baja is a bi-directional pipeline;

100% of Tuscarora, a 305-mile pipeline that extends between the GTN pipeline near Malin, Oregon to its terminus near Reno, Nevada and delivers natural gas in northeastern California and northwestern Nevada.

For the most recent quarter, the partnership reported net income of $31 million, down $6 million from the same period a year ago primarily due to the cost of acquiring the 30% of Bison that it didn’t already own. The cash distribution rose from $0.81/unit a year ago to $0.84/unit, which translates into a 4.6% annualized yield at the current price.

Another gas pipeline partnership among the top five year-to-date MLP performers is Tallgrass Energy Partners (NYSE: TEP). Tallgrass provides natural gas transportation and storage services for customers in the Rocky Mountain and Midwest regions of the US. The partnership launched in May 2013, and unlike many of the MLP IPOs of recent years, units traded pretty flat for the first four months. After notching a modest gain in 2013, the unit price caught fire, and Tallgrass been one of the brightest spots this year among MLPs with a total return of 64% YTD.

Tallgrass assets include:

Tallgrass Interstate Gas Transmission (TIGT) Pipeline, a FERC-regulated natural gas transportation and storage system with 4,645 miles of gas transportation pipelines serving Wyoming, Colorado, Kansas, Missouri and Nebraska with natural gas primarily coming from the Denver-Julesburg Basin and the Niobrara and Mississippi Lime shale formations. The TIGT System also includes the Huntsman natural gas storage facility in Nebraska;

Trailblazer Pipeline system, a 439-mile interstate pipeline with a capacity of up to 862 million cubic feet per day (MMcf/d) that transports natural gas from southeastern Wyoming to interconnections with the Natural Gas Pipeline Company of America and Northern Natural Gas Company pipeline systems in Nebraska;

Natural gas processing plants in Casper and Douglas, Wyoming with a combined processing capacity of approximately 190 MMcf/d;

A natural gas treating plant in West Frenchie Draw, Wyoming.

For the third quarter of 2014, Tallgrass reported adjusted EBITDA of $23.7 million, a 37% increase over the third quarter of 2013. The partnership declared a quarterly cash distribution of $0.41 per common unit, which translates to a 4.2% annualized yield at the current price. This amount was 42.6% over TEP’s minimum quarterly distribution, and the $3.2 million in distributable cash flow represented a coverage ratio of 1.15.

(Follow Robert Rapier on Twitter, LinkedIn, or Facebook.)

Portfolio Update

EQT Midstream Tallies Cost of Growth

The good news for EQT Midstream (NYSE: EQM) is that gas-centered drilling in the Marcellus remains largely impervious to plunging oil prices, and that demand for midstream infrastructure in the basin will support its newly announced capital spending plan worth an estimated $380 million to $410 million in 2015.

The bad news is that half of the returns on those investments will be indefinitely skimmed by the MLP’s general partner.

The good news is that the yield is up to 2.7% following the 19% decline from June’s record high, including Monday’s 8% wilt amid broad MLP weakness.

That, of course, sounds a lot like bad news, as does the fact that even after its steep drop EQM continues to be valued at some 30 times trailing EBITDA (adjusted earnings) based on its enterprise value.

But then that’s par for the course for fast-growing MLPs, and EQM is certainly one of those, its revenue and per unit distribution still rising more than 20% annually. The payout growth is expected to slow in the coming years, though, as the general partner’s increased skim takes its toll.

In any case, EQM sponsor EQT (NYSE: EQT) on Monday revealed plans to spin off its general partnership interest in EQM into a separate affiliate, which would go public with an MLP representing a minority stake in that general partner interest sometime next summer. The new GP MLP would very likely enjoy a higher valuation multiple than EQM, to say nothing of EQT. As for EQM, it remains a Hold. I’ll have more on the best way to capitalize on its growth in next week’s MLP Profits issue.

— Igor Greenwald

Stock Talk

Tom Light

Igor-

If we ever needed a “bone” we sure need it now-any clue on release of the next issue?

Thank you for all of the good work that you and all of the team do for us!

This has been a real trying few weeks-

You must be logged in to post to Stock Talk OR create an account

Add New Comments

You must be logged in to post to Stock Talk OR create an account